Thursday, July 30, 2015

Tuesday, July 14, 2015

8 Markets Topping Pre-Housing Crisis Peaks

Read more: Real Estate and the Middle ClassA handful of housing markets, seeing hefty home price increases, have zoomed ahead of their previous pre-housing crisis peaks in the past year. RealtyTrac crunched numbers from its February 2015 U.S. Home Price Appreciation Analysis to identify the top markets that have exceeded their previous peaks.

The following markets topped its list, surging to new home price peaks (included below with the dollar amount of the 2005 to 2015 peak price):

- San Jose-Sunnyvale-Santa Clara, Calif.: $714,750 (June 2014)

- Austin, Texas: $300,000 (September 2014)

- Denver, Colo.: $265,000 (July 2014)

- Raleigh, N.C.: $198,000 (July 2014)

- Nashville, Tenn.: $175,000 (August 2014)

- Charlotte-Gastonia-Concord, N.C.-S.C.: $173,000 (July 2014)

- Columbus, Ohio: $154,000 (August 2014)

- Oklahoma City, Okla.: $135,000 (August 2014)

Friday, July 10, 2015

Maintenance Adds Surprise Costs to Homeownership

Heating and cooling bills, regular maintenance tasks, and system updates can put a dent in your finances.

When most people — particularly

first-time home buyers — think about the costs associated with

purchasing a home, they typically consider the costs related to closing

on the deal. These closing costs include mortgage, title and insurance

fees.

What many homeowners don’t plan for are the costs associated with actually owning the home. If you are buying a home that needs work, you would get estimates and build those expenses into the overall cost of owning the home. But there are more expenses, even for homes that are in move-in condition.

Many home buyers focus much of their attention on the purchase price or the interest rate of the loan. In reality, saving $10,000 on the overall purchase price or getting a 1/8-point lower on the loan won’t translate into cash in your pocket. But hidden expenses — those that come with the territory of homeownership — will certainly affect your finances.

But to heat a home in the Northeast through the winter, you’ll need an oil truck to deliver 150 gallons of oil to your home every five weeks — to the tune of $800 per fill up. And don’t be surprised by an extra $100 per month on your electric bill from May to October if you are using air conditioners. The average consumer, without knowledge of these day-to-day realities, will face severe sticker shock.

Similarly, if you move from the suburbs to the country, expect a septic system and well water. Each of these requires regular maintenance and expenses.

If you negotiate a $5,000 price reduction, that’s great. But it won’t help for cash flow purposes. That slight reduction, amortized over the life of the loan, may translate into savings of less than $50 per month. Wouldn’t you rather have that money in your pocket at the closing?

As a part of your home buying due diligence, understand from the property inspector what is required to maintain the home. Most buyers think that the inspection is all about finding faults or issues with the property. While poking holes in the home is certainly one aspect of inspecting, what’s just as important is having the opportunity to learn about the home and its systems.

Use the walkthrough with a licensed inspector and the written report to identify what home improvement issues you will face. Budget and plan for a two-, three- or five-year plan to address issues like a leaky water heater, energy-inefficient single pane windows or a boiler near the end of its usable life.

What many homeowners don’t plan for are the costs associated with actually owning the home. If you are buying a home that needs work, you would get estimates and build those expenses into the overall cost of owning the home. But there are more expenses, even for homes that are in move-in condition.

Many home buyers focus much of their attention on the purchase price or the interest rate of the loan. In reality, saving $10,000 on the overall purchase price or getting a 1/8-point lower on the loan won’t translate into cash in your pocket. But hidden expenses — those that come with the territory of homeownership — will certainly affect your finances.

Relocating from one part of the country to another?

Someone moving from Northern California to the suburbs of Connecticut will be blown away to learn how expensive it is to own a home. If you live in an area where air conditioning isn’t necessary, and heat comes from gas-fired HVAC systems, your month utility bills and the regular costs associated with homeownership will be relatively low.But to heat a home in the Northeast through the winter, you’ll need an oil truck to deliver 150 gallons of oil to your home every five weeks — to the tune of $800 per fill up. And don’t be surprised by an extra $100 per month on your electric bill from May to October if you are using air conditioners. The average consumer, without knowledge of these day-to-day realities, will face severe sticker shock.

Similarly, if you move from the suburbs to the country, expect a septic system and well water. Each of these requires regular maintenance and expenses.

Ask for credits instead of a lower purchase price

To manage these maintenance costs, it’s smart to set some money aside, and one way to do that is to get a credit when you buy the home. Most lenders will allow buyers a credit back from the seller at the closing, up to 6 percent. A reduction structured as a credit back cuts your closing cost expenses and keeps money in your pocket to earmark for home improvement.If you negotiate a $5,000 price reduction, that’s great. But it won’t help for cash flow purposes. That slight reduction, amortized over the life of the loan, may translate into savings of less than $50 per month. Wouldn’t you rather have that money in your pocket at the closing?

Use your inspection to establish a home maintenance plan

Part of becoming a homeowner is performing regular maintenance. You can’t call your landlord to fix problems once you own a home.As a part of your home buying due diligence, understand from the property inspector what is required to maintain the home. Most buyers think that the inspection is all about finding faults or issues with the property. While poking holes in the home is certainly one aspect of inspecting, what’s just as important is having the opportunity to learn about the home and its systems.

Use the walkthrough with a licensed inspector and the written report to identify what home improvement issues you will face. Budget and plan for a two-, three- or five-year plan to address issues like a leaky water heater, energy-inefficient single pane windows or a boiler near the end of its usable life.

Know before you go

If you are moving to a new area — whether it is only five miles away or five thousand miles — find out at the beginning of the home-buying journey what to expect once you are a homeowner. Do your due diligence on home improvement and maintenance just as you would school districts or housing stock.Tuesday, July 7, 2015

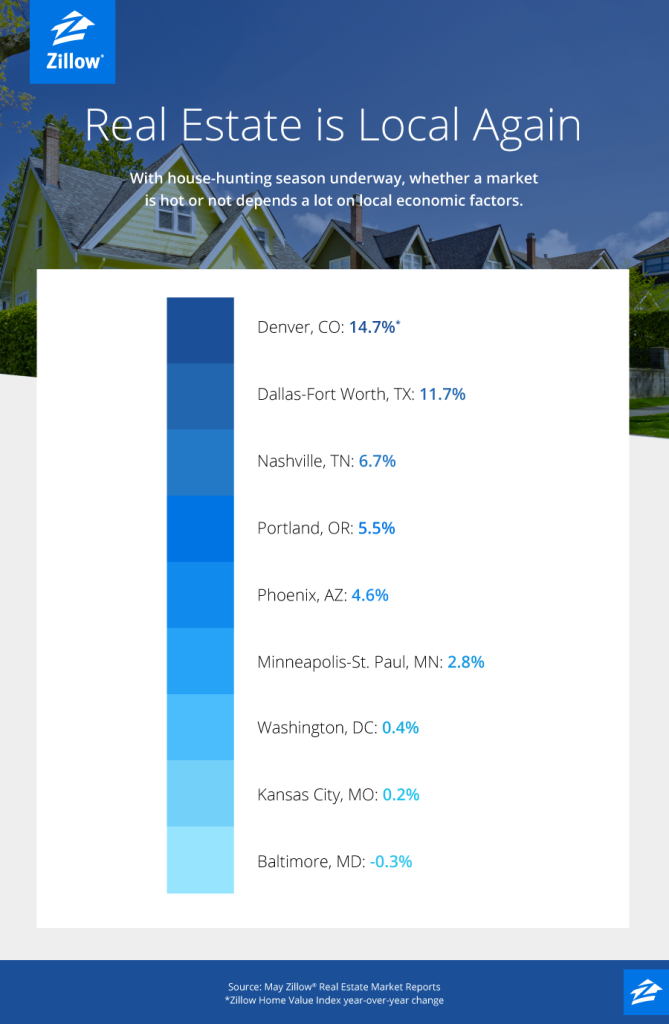

Real Estate is Local Again

Instead

of riding the wave of recovery, individual housing markets are

responding to their local economics this home-buying season.

Double-digit home-value growth is

setting records in Denver, San Jose, Dallas and San Francisco this

home-buying season. The housing market is much cooler in Florida, with

home values in Tampa, Miami-Fort Lauderdale and Orlando growing at half

the pace they were one year ago.

The May Zillow Real Estate Market Reports highlight the country’s diverging real estate markets. After years of riding the same big roller coaster through the housing bubble, bust and recovery, local housing markets took home buyers and sellers on different rides this spring.

Nationally, home value growth has cooled, slowing to a rate of three percent year-over-year. Rents are growing faster: the median national rent is up 4.5 percent over the past year.

The slowing, diverging market is a sign of recovery, said Zillow Chief Economist Stan Humphries. And it means real estate is local again.

“What we’re seeing is the passing of the baton — as mortgage rates begin to rise, and incomes and household formation rates increase — from a stimulus-driven housing market to one driven by fundamentals,” Humphries said.

First-time home buyers are returning to the market, and by the end of 2015, Humphries expects the millennial generation to displace Generation X as the largest group of home buyers.

Home values growth is expected to slow even further in the next year, to an annual rate of 2.2 percent.

For more information about Zillow’s monthly report, check out Zillow Research.

The May Zillow Real Estate Market Reports highlight the country’s diverging real estate markets. After years of riding the same big roller coaster through the housing bubble, bust and recovery, local housing markets took home buyers and sellers on different rides this spring.

Nationally, home value growth has cooled, slowing to a rate of three percent year-over-year. Rents are growing faster: the median national rent is up 4.5 percent over the past year.

The slowing, diverging market is a sign of recovery, said Zillow Chief Economist Stan Humphries. And it means real estate is local again.

“What we’re seeing is the passing of the baton — as mortgage rates begin to rise, and incomes and household formation rates increase — from a stimulus-driven housing market to one driven by fundamentals,” Humphries said.

First-time home buyers are returning to the market, and by the end of 2015, Humphries expects the millennial generation to displace Generation X as the largest group of home buyers.

Home values growth is expected to slow even further in the next year, to an annual rate of 2.2 percent.

For more information about Zillow’s monthly report, check out Zillow Research.

Friday, July 3, 2015

3 Extreme Home-Buying Tactics to Get the House You Want

What can you do if you fear the seller of your dream house will go with another buyer … or if they already have?

Today, in many markets, homes move

quickly, often with multiple offers. Some homes, called “pocket

listings,” sell before even hitting the market. It can be an all-out war

for competitive buyers, and some will go to great lengths to win.

Here are three tips for going the extra mile to make sure you come out the winning bidder.

When all else fails, it’s time to move on. There will be another house — there always is. Take the loss and chalk it up to experience. When the next great house comes along, be the first to see it, get the first offer in the door and make your offer irresistible.

Here are three tips for going the extra mile to make sure you come out the winning bidder.

Make your offer a “sharp” offer

If the market is competitive and you really want the home, you need to let the seller know you’ll do whatever it takes to win it. In some cases, buyers will make what we call a “sharp” offer. In this situation, a potential buyer will match the highest and best offer, and raise that offer price by five percent — or sometimes even 10 percent.Offer to buy out the winning buyer

I’ve seen remorseful buyers, frustrated after losing out in a bidding war, track down the winning buyer and negotiate with them. In this scenario, the losing buyer offers to pay the winning buyer their earnest money deposit (sometimes up to three percent of the purchase price) plus any expenses, in return for letting them take over the purchase.Write a letter to the new homeowners once they close

If you can’t try to snag the home from the wining bidder, there is one final option. Knock on the door or write a letter to the new owner. Explain that you missed out on the home and that you would like to purchase it directly from them. In this case, you’d have to make them an incredible offer — one that would cover their sales and moving costs, and put money in their pocket. If you hit the right number, you just might motivate them.When all else fails, it’s time to move on. There will be another house — there always is. Take the loss and chalk it up to experience. When the next great house comes along, be the first to see it, get the first offer in the door and make your offer irresistible.

Subscribe to:

Posts (Atom)